O&G From Federal Lands

O&G From Federal Lands

Looking at sources and trends

As part of Biden’s proposed reconciliation directive, there are several new changes targeting Oil & Gas production on federal lands, from the way lease sales are done, to royalty rates, and other additional fees.

Given this backdrop, I though it was time to dig a bit deeper into the data to see where production comes from, how much money it makes, and where it goes.

Production

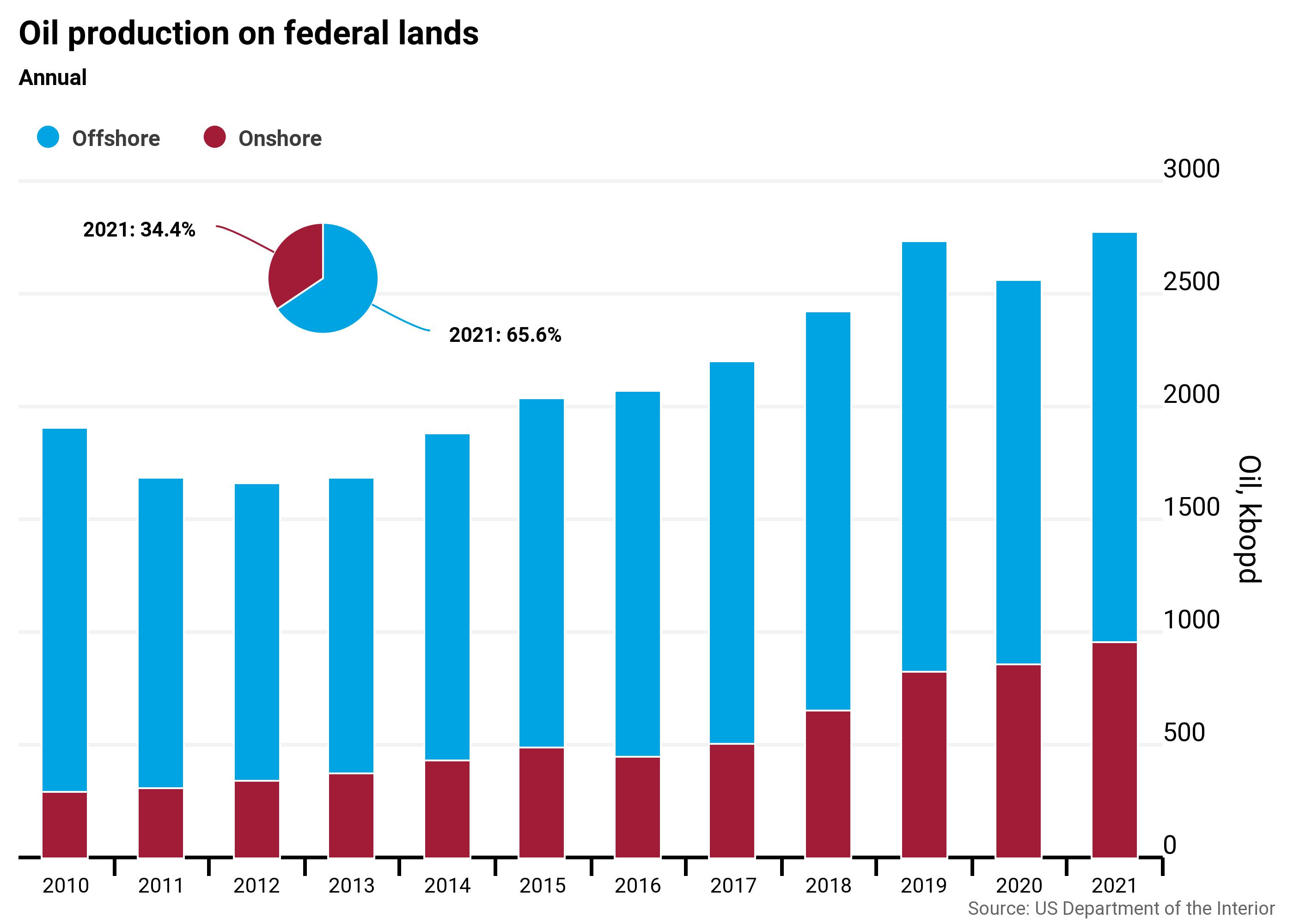

In 2021, oil production from Federal lands is reaching all time highs (~2,800 kbopd) after a dip in 2020. This is largely being driven by New Mexico oil production increases.

Gas continues to decline after years of low prices/investment.

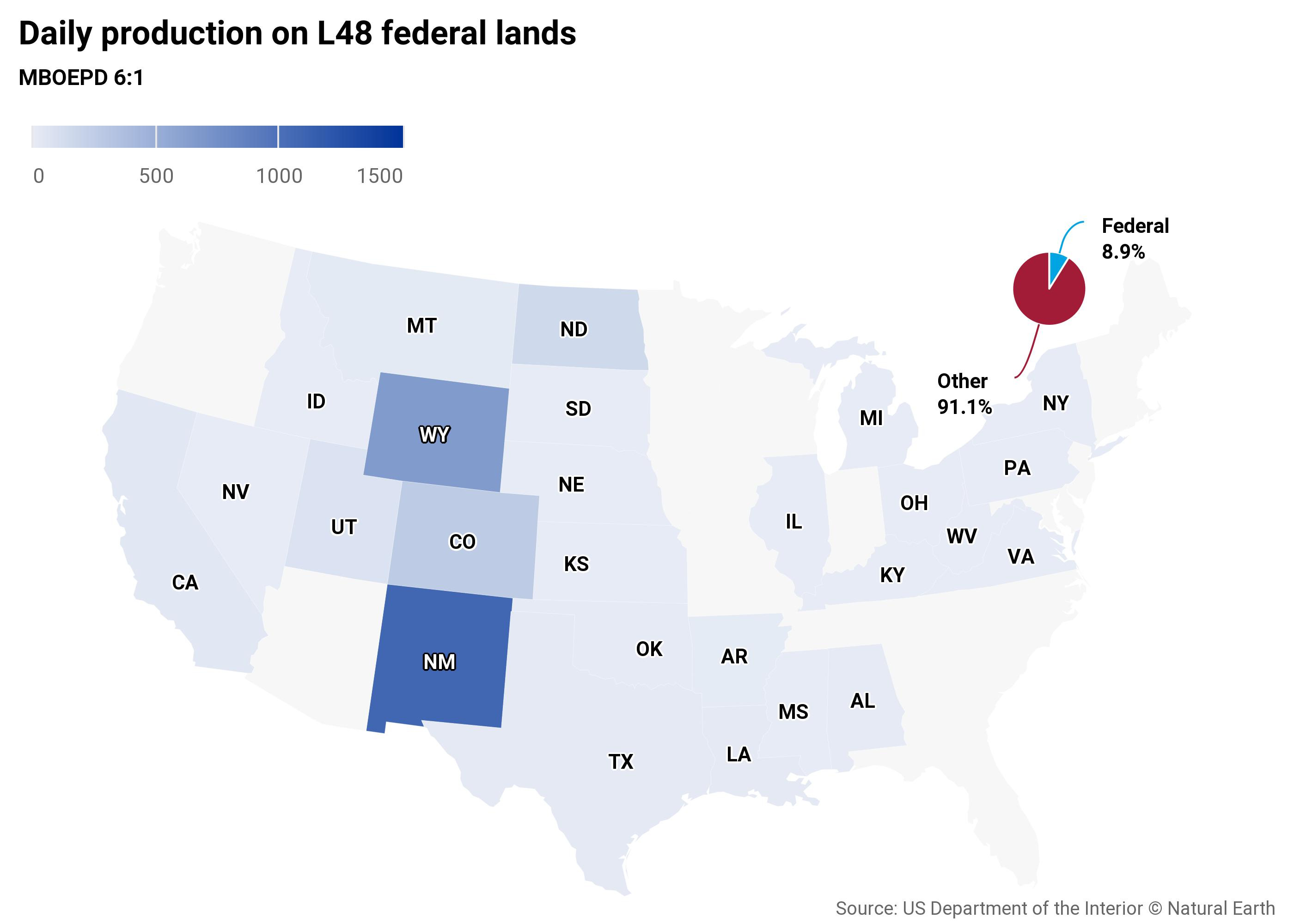

While all Federal waters are feeding the coffers of the Governent, onshore L48 has ~9% of total production share, due to the glories of Private Ownership. Total Alaska is around 0.8% Federal.

Most of L48 is focused on New Mexico and Wyoming, where ~50% of total production is on Federal lands. Together, these two states represent ~75% of L48 onshore Federal boe equivalent production.

Eddy and Lea counties in New Mexico are the focus of the Delaware Wolfcamp, the most active current play in the US. In 2020, roughly 38% of all onshore L48 Federal boe equivalent production came from those two counties.

Wyoming is home to the Powder River Basin, which is a pretty active basin itself. However, Wyoming is here largely because the entire state is peppered with Federal leases. Wyoming had about 28% share of total BOE’s produced.

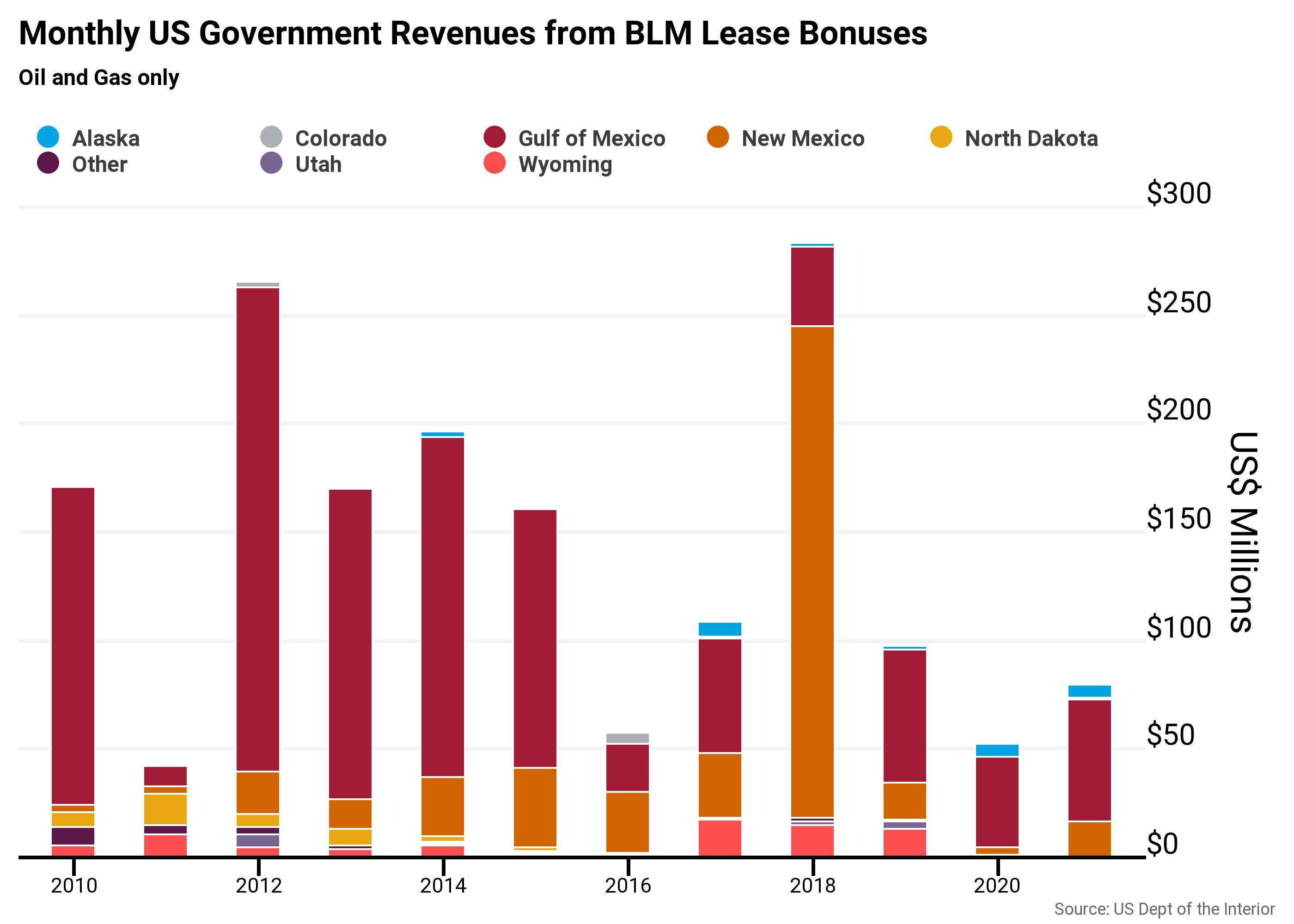

Revenues

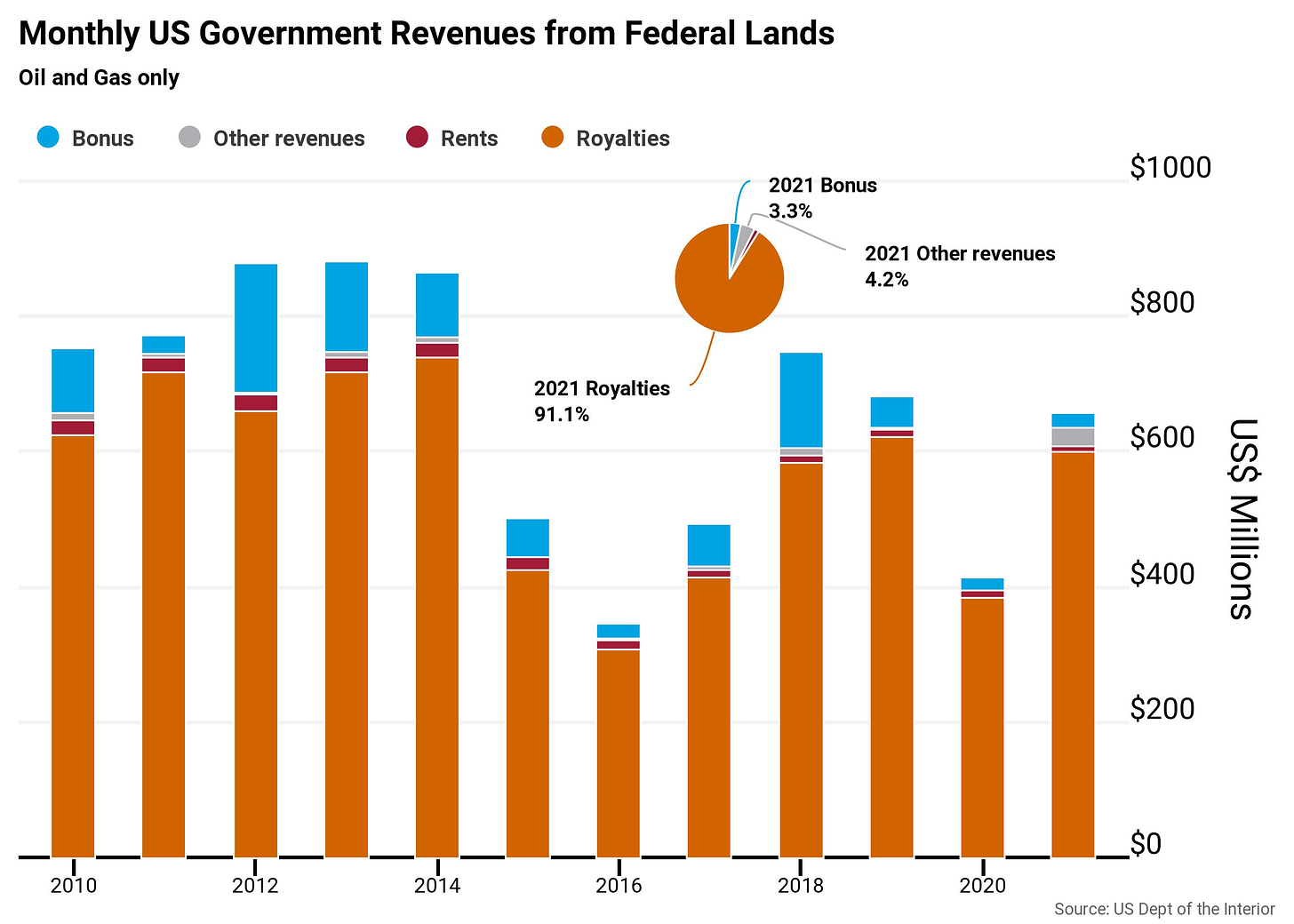

Federal lands make revenue through a few avenues:

Royalties - Historical terms on leases are 12.5% royalty on a 10-year term.

Rents - Annual rental rates for both competitive and noncompetitive leases are $1.50 per acre (or fraction thereof) in the first 5 years and $2.00 per acre each year thereafter.

Bonus - Lease bonus payments during BLM lease sales.

Fees/Other Revenues - Inspection fees and ancillary other are a small protion of total.

The US government spent approximately $545 Billion a month in 2020, so looks like Federal O&G leases are funding around 0.075% of the total budget.

Royalties make up the vast majority of revenue, though it is the most variable as it is tied to the commodity price. Of course, bonus payments have been on a steady down-trend since the Permian-fueled bonanza back in 2017/18.

Offshore leasing was very strong in the high-price days of 2012-2014, but has fallen with prices. If the current environment persists, I think we’ll see an uptick in GoM leasing again.

Eddy and Lea counties once again represent a huge share so far in 2021, with ~27% of total revenue to date, and a ~58% of total L48!

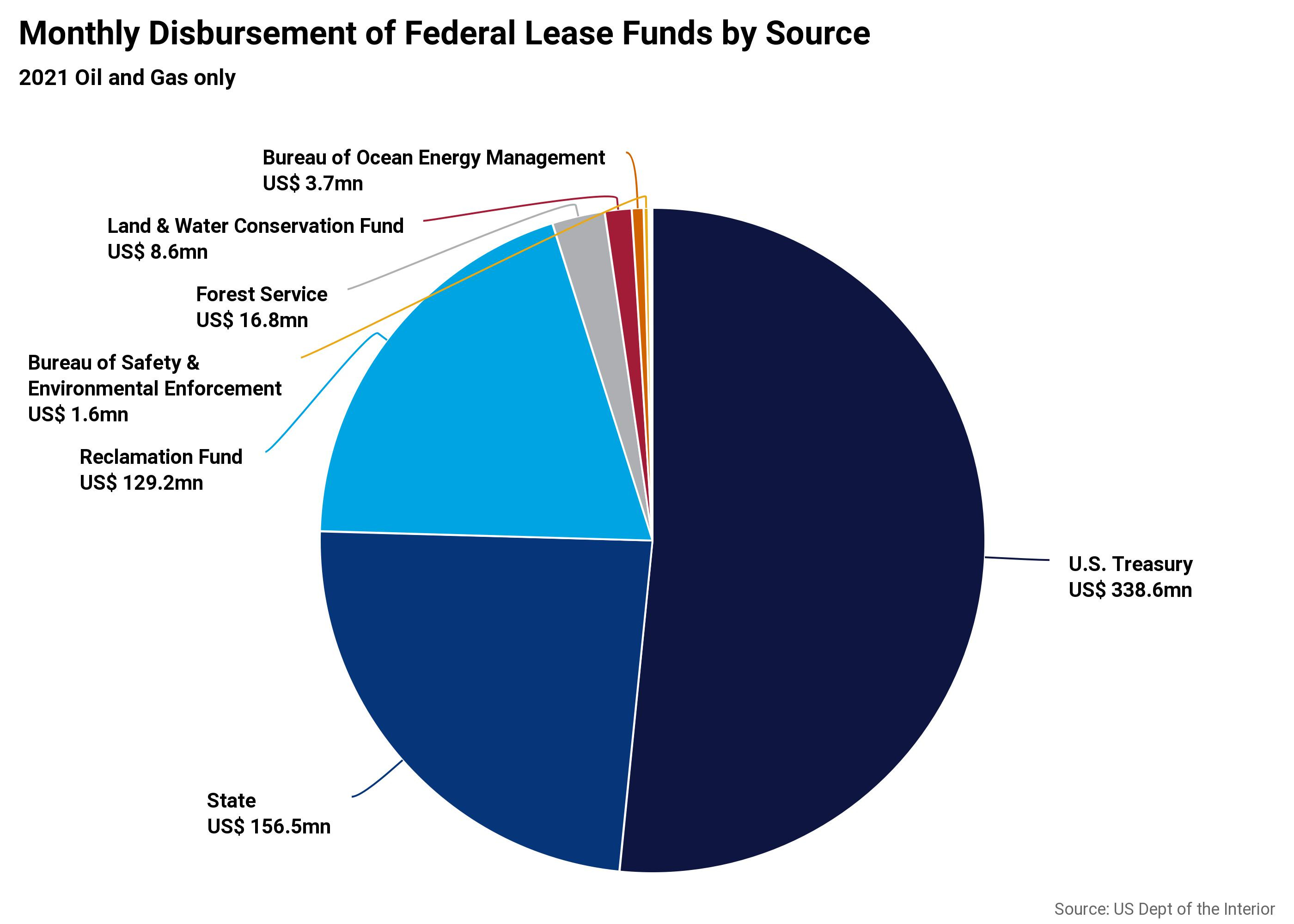

Disbursements

Where did the cash go? A goodly portion heads back to the enforcement agencies and wildlife/conservation funds. Over half goes to the US Treasury, while State coffers get about a quarter.

The Reclamation Fund gets a huge amount of this cash. What is it?

The Reclamation Fundlargely supports irrigation and hydropower projects overseen by the Bureau of Reclamation.

The Reclamation Fund was created through The Reclamation Act of 1902. The fund was originally designed to support irrigation projects in the western United States, and its funding came primarily from the sale of federal land and timber. Over the years, Congress explored new revenue sources for the fund, and expanded the projects the fund was authorized to support.

So, while the US Treasury soaks up a good portion of this cash, a large portion does seem to be supporting some pretty good causes. That’s right folks, O&G is doing good out there!

Summary

Bit interesting to see where the funds come from and where they’re headed. Looks like two counties in New Mexico are funding the vast majority of Federal Lease Disbursements!

For my paid subscribers, I’ll be digging in to the proposed changes by the Biden admin and look at some various statistics that can be pulled from the data.